On December 3-5, 2014, the Institute of Politics at Harvard University held its biannual Bipartisan Program for Newly Elected Members of Congress. Most of the congress-people come. This year I was on a panel on the domestic US economy, titled the “Middle Class Crunch.” In Part I, presented here, I briefly reviewed recent economic statistics. Part II, laying out 8 recommended policies, will follow.

The standard economic statistics indicate that the US economy has been doing well lately, not just relative to the severe 2007-09 recession, but relative also to what most Americans think and relative to how other advanced countries are doing. This applies to (1) GDP, (2) jobs, (3) the stock market, and (4) the budget.

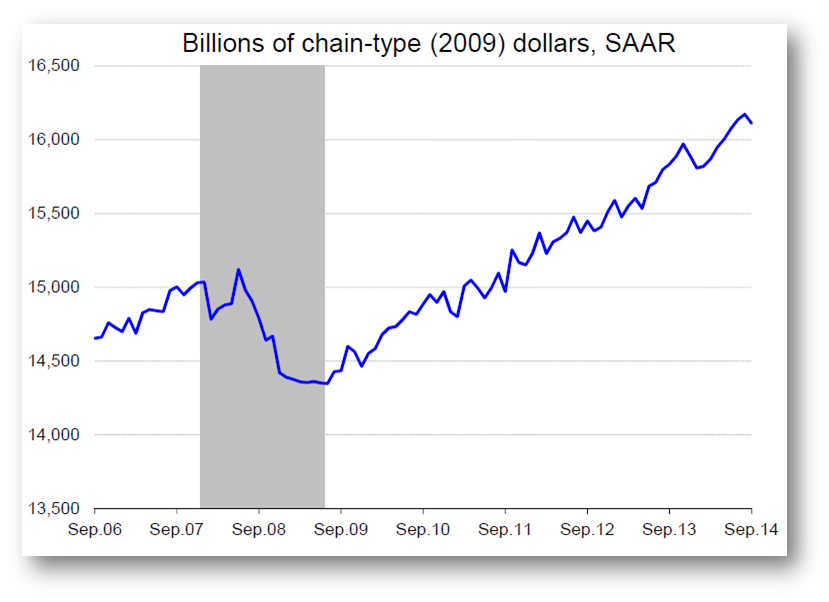

(1) GDP growth has averaged an impressive 4.2% over the last 2 quarters. It has averaged a more moderate 2.4% over the last 4 quarters, but even that is still above the disappointing 2.1% in 2011-13. See Figure 1.

Figure 1. Growth has been gradual since the recession’s end in June 2009, but faster lately

Source: Macroeconomic Advisers, Nov. 18, 2014; monthly numbers derived from US Bureau of Economic Analysis quarterly series. E

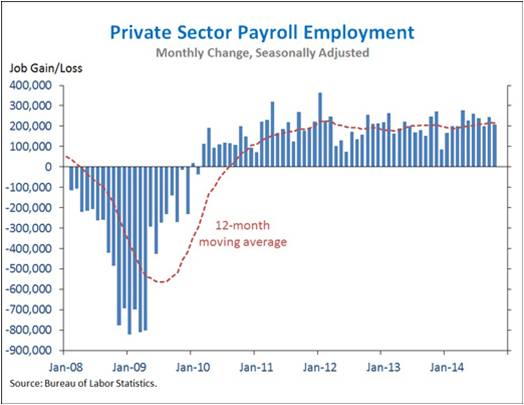

(2) Employment growth has shown an unprecedented string of positive numbers. The private sector has added 10.6 million jobs over 56 straight months of job growth, easily the longest streak on record. and has added at least 200,000/mo. for nine consecutive months. See Figure 2.

Figure 2. Change in private sector employment.

(3) The stock market is setting record highs.

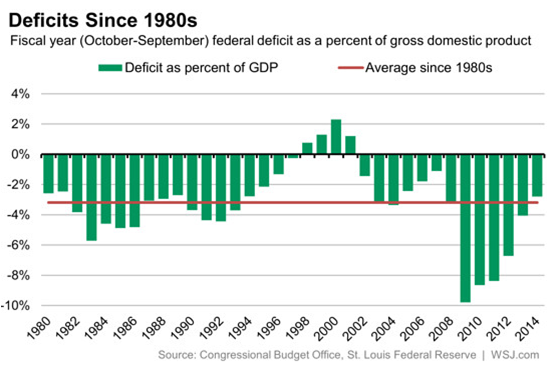

(4) The budget deficit has experienced a record improvement since 2009: a decline of more than 2/3. (See Figure 3.) It is now 2.8% of GDP, which is below the average deficit since 1980 (3.2%).

Figure 3. The 2014 federal budget deficit is down to 2.8% of GDP.

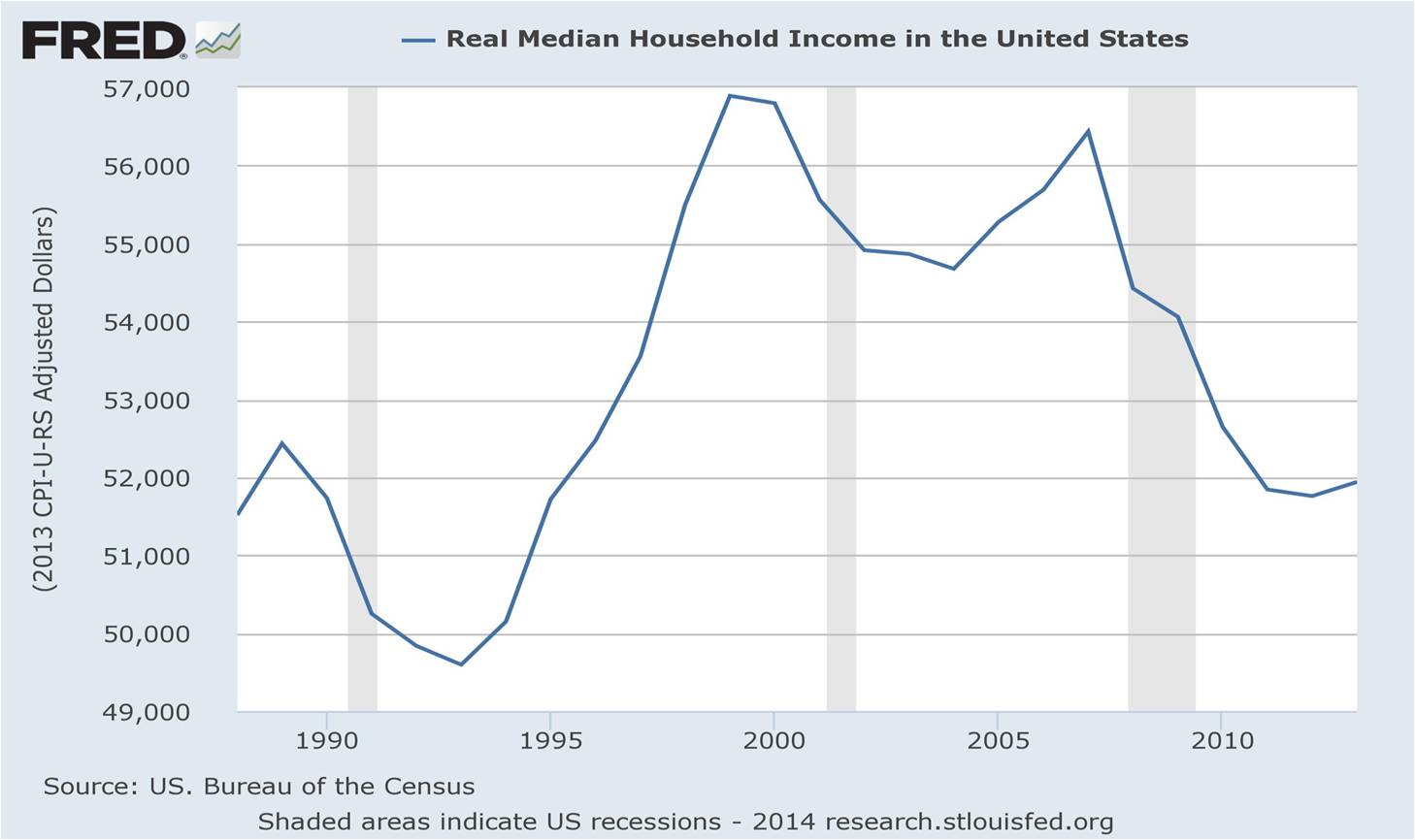

If the economy is doing so well, then why don’t Americans see it that way? The “middle class” doesn’t feel better off because the gains have accrued to people at the top. Median family income is still 8 per cent below its pre-recession level and even further below its 2000 peak. It has barely risen above its 1990 level. See Figure 4.

Figure 4. Real median household income is barely above its 1990 level.